Macroprudential liquidity tools for investment funds – A preliminary discussion

Published as part of the Macroprudential Bulletin 6, October 2018.

This article aims to facilitate discussion on potential macroprudential tools for investment funds. To this end, the article puts forward an initial assessment based on the application of a conceptual framework and aims to inform the debate on the potential design aspects of macroprudential liquidity tools. In line with the ESRB’s approach to developing macroprudential instruments, the effectiveness and efficiency of various macroprudential liquidity tools for investment funds are thoroughly assessed. The article provides an overview of the various liquidity tools and assesses the suitability of these tools for containing the materialisation of systemic risks through various channels.

1 Introduction

The investment fund sector has expanded rapidly over the past decade, with signs of increased risk-taking. Between 2008 and the end of 2016 total net assets of European funds more than doubled from €6.1 trillion to €14.1 trillion. During this period, funds increased their investments in riskier and less liquid assets, while at the same time offering short-term redemptions to investors.[1]

Policymakers at the global and European levels have expressed concerns about financial stability risks that may stem from investment funds. [2] In the light of the need to better monitor and address potential financial stability risks, the Financial Stability Board (FSB) in 2017 published policy recommendations to address vulnerabilities arising from asset management activities. Importantly, FSB Recommendation 8 delineates a potential macroprudential role for authorities in providing direction on the use of liquidity risk management tools by funds in extraordinary circumstances. [3] The FSB states that authorities need to be equipped with relevant powers to be able to mitigate structural vulnerabilities arising from asset management activities, in particular for situations where measures available to asset managers alone would not be sufficient.

The European Systemic Risk Board (ESRB) also advocates exploring further the use of current liquidity management tools for macroprudential purposes. A key short-term task highlighted by the ESRB is to contribute to the development of new macroprudential instruments beyond banking, including instruments that address liquidity mismatches for investment funds.[4] In the light of the rapid expansion of the investment fund sector which has been accompanied by initiatives to move to a more market-based financial system, authorities need to be provided with instruments to prevent or mitigate new systemic risks arising from this structural shift in the financial system.

While fund managers’ liquidity management tools may mitigate liquidity risk under many foreseeable scenarios, they might not be sufficient to address macroprudential vulnerabilities. This is because managers of individual funds have a mandate to act in the best interests of their own investors, not to assess their potential contribution to systemic risk, and may not be in a position to act in the interest of financial stability. Similarly, supervisors of individual funds may not have the mandate and information necessary to properly assess different funds’ contribution to systemic risk and may therefore also not be properly equipped to address systemic risk.

This article aims to inform the debate by facilitating discussion on potential macroprudential tools for investment funds. In this article, macroprudential liquidity tools for investment funds are conceptually assessed thoroughly following ESRB guidance to develop macroprudential instruments. [5] Importantly, the ESRB advises that authorities use a macroprudential policy strategy comprising (i) risk identification and monitoring, (ii) the definition of intermediate objectives for financial stability, and (iii) the design of instruments that are effective and efficient in meeting the intermediate policy objectives. [6] The focus of this article is to further facilitate discussion on point (iii) by analysing the effectiveness and efficiency of various macroprudential liquidity tools for investment funds. First, the article provides an overview of the different channels through which systemic risk may materialise. Second, it provides an overview of various liquidity tools and assesses the effectiveness of these tools in addressing the risk of fire sales, spillovers to other financial counterparties and disruptions in credit intermediation. Third, it assesses whether tools are proportional and sufficiently simple, and whether they are able to contain unintended consequences, which are essential criteria for a macroprudential tool to be considered efficient.

2 Liquidity and systemic risk

The risk of investor runs is a key vulnerability that stems from liquidity mismatches in open-ended funds. [7] A mismatch between the liquidity of a fund’s assets and the liquidity offered to investors through the fund’s redemption policies gives rise to first-mover advantages. If investors anticipate severe losses on the fund’s investments, they could be incentivised to “run for the exit” to be the first to redeem their shares. Fund managers have to sell assets to meet redemption requests. The stressed sale of assets could pose a negative externality to the financial system. The first-mover advantage in open-ended funds arises because losses on asset sales to meet redemptions are incurred by investors which remain in the fund. If a sufficiently large number of investors anticipate and respond to the redemption behaviour of other investors, the potential to disrupt financial stability increases. Competition may incentivise fund managers to offer short-term redemptions to signal their quality and attract investors. This competitive pressure may lead to an excessive offering of short-term access to liquidity and an increase in the risk of investor runs.

Run risk is higher for funds with large liquidity mismatches and funds that use leverage. Because selling illiquid assets is more costly than selling liquid assets, investors have a greater incentive to run from funds that invest in illiquid assets. [8] Leverage, through direct borrowings or derivatives, also amplifies the risk of runs[9] leveraged open-ended funds experience greater investor outflows after bad performance than unleveraged funds, based on a large sample of European alternative investment funds. Following substantial outflows, investors in leveraged funds may perceive significant selling pressures on these funds since the funds need to adjust their portfolios more than unleveraged funds, forcing them to conduct unprofitable trades which can lead to greater valuation losses.

The risk of sudden spikes in margin calls is another type of liquidity risk that has the potential to contribute to systemic risk. The use of derivatives inter alia allows fund managers to obtain more economic exposure than would be possible if the funds only invested in the underlying assets. Derivatives can make funds more sensitive to market movements and can lead to sudden margin calls which need to be paid in cash. Unexpected spikes in margin calls could force the fund to sell off assets. Margin calls are more problematic if funds invest in illiquid assets, or if funds offer short-term redemptions. [10] In this sense, the risks of liquidity mismatches and leverage in funds are closely linked.

The sale of assets to meet investor redemptions or margin calls may contribute to systemic risk through the following transmission channels:

- Fire sales: The forced sale of assets may dislocate prices and reduce liquidity in financial markets. Fire sales pose negative externalities for other financial institutions, for example in the form of valuation losses on investments, higher margin and haircut requirements, or even increased default probabilities. In extreme scenarios, these indirect spillovers may leave financial institutions more liquidity-constrained, which could lead to further funding and market illiquidity, and disruption in financial intermediation.

- Direct spillovers to other financial institutions: Liquidity problems in investment funds could also result in direct losses for financial institutions which invest in the funds. In addition, many funds are owned by institutions like banks, insurance companies or pension funds. In some cases, these fund owners may also extend liquidity support to distressed funds. This could be in the form of guarantees or committed credit lines, but support could also be extended ad hoc for fear of reputational damage for the fund and its owner. Finally, losses could be transmitted to financial institutions that act as a counterparty in repo or derivative transactions.

- Disruptions in credit intermediation: Funds invest in credit instruments such as bonds and commercial paper and thereby provide funding to the non-financial sector. If funds suddenly sell their investments in such instruments to meet liquidity needs, this can disrupt the funding possibilities for the issuers of the debt securities. Such a risk is particularly important for issuers that rely on short-term market financing and have limited alternative funding options. As mentioned previously, this effect is amplified if other financial institutions that invest in the same credit instruments also become more liquidity-constrained in a fire-sale scenario with dislocated markets.

3 Effectiveness and efficiency of macroprudential liquidity tools

The FSB and ESRB have called for an exploration of the role of authorities in addressing systemic vulnerabilities stemming from liquidity mismatches in investment funds. The FSB recommends that authorities consider providing direction on the use of liquidity management tools by fund managers in exceptional circumstances. The ESRB[11] identified the development of macroprudential instruments that address liquidity mismatches at investment funds as a key priority for the short to medium term, and has recently called for further guidance on the power of authorities to suspend redemptions.[12] To date, the suspension of redemptions is the only liquidity instrument available to authorities in Europe. [13]

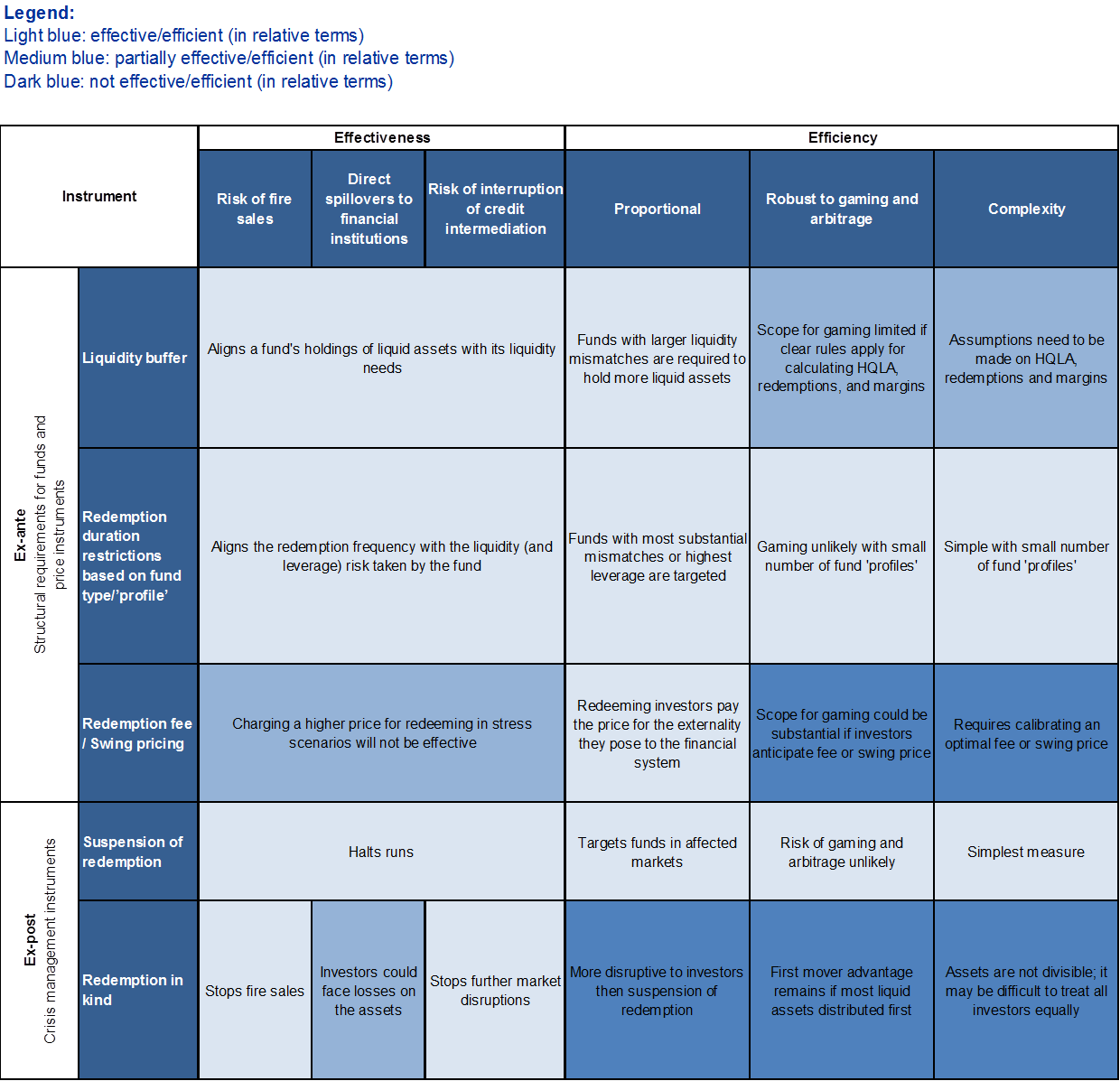

This section aims to contribute to the international policy debate in this area, by providing a preliminary conceptual assessment of the effectiveness and efficiency of several potential macroprudential liquidity instruments. The framework used facilitates an assessment of various potential measures in line with the ESRB’s approach[14] to developing macroprudential instruments, and has previously been applied to assess the possible design options for macroprudential leverage limits for alternative investment funds (see Table 1).[15] The assessment aims to inspire further analysis on the need for macroprudential liquidity instruments and informs the debate on possible instrument design aspects.

To be effective, a macroprudential liquidity measure for investment funds should limit the extent to which liquidity mismatches contribute to fire sales, direct spillovers to other financial institutions and disruption in credit intermediation. By addressing these externalities, the liquidity instruments would contribute to the ESRB’s financial stability objective to mitigate the risk of “excessive liquidity or maturity mismatch and market illiquidity”.

A macroprudential liquidity instrument can be deemed efficient if it is simple in its implementation, its impact is proportional to the risk, and its unintended consequences are contained. A straightforward and easy-to-calibrate instrument improves transparency and helps to avoid inaction bias. For any measure taken, the costs and benefits should be weighed against each other, and the measure should be proportional to the risks addressed. In this respect, it is important to take into account any potential unintended consequences of a measure, including cross-border spillovers and gaming or arbitrage opportunities.

The diversity of business models – and associated vulnerabilities – in the investment fund sector may warrant a differentiated approach. A one-size-fits-all approach may not be effective since vulnerabilities may stem from different types of liquidity risks (e.g. some funds may be susceptible to run risks, while other funds are prone to sudden spikes in margin calls). Moreover, such an approach may not be efficient because the implementation of a one-size-fits-all measure may make some fund types unviable.

The selection of potential macroprudential liquidity instruments in this section is guided by the liquidity management tools that are available to fund managers. Broadly speaking, fund managers’ liquidity management tools can be categorised as pre-emptive (ex-ante) or post-event (ex-post) measures. Pre-emptive measures are meant to improve the resilience of funds to redemptions and other liquidity shocks, thereby limiting the funds’ contribution to the build-up of systemic risk. Pre-emptive measures include, for example, the alignment of the investment strategy, asset liquidity and redemption policies. Redemption policies pertain to the frequency at which investors are allowed to redeem, notice periods and lock-up periods. Fund managers can also use price-based measures such as redemption fees or swing pricing to address first-mover advantages and to smooth flows into and out of the fund. Post-event measures can be activated if the liquidity risk of a fund materialises or is imminent. Post-event measures include tools such as redemption in kind or the suspension of redemptions. Such measures can be used by fund managers in exceptional circumstances to minimise stressed outflows from the fund and can be considered as a crisis management instrument.[16]

With a view to improving the resilience of funds, it may be worthwhile further exploring structural requirements such as liquidity buffers or redemption duration restrictions. A liquidity buffer would require funds to hold sufficient high-quality liquid assets (HQLA) to meet redemptions, margin calls, and other outflows at any time including stressed market conditions for an extended period of time. The requirement may effectively address funds’ potential contribution to systemic risk by making them more resilient to investor runs and/or spikes in margin calls. A liquidity buffer concept could be operationally feasible, since such a requirement has already been implemented for the banking sector.[17] Yet, the identification of high-quality liquid assets and the estimation of margin requirements and redemptions may be relatively complex.[18] Alternatively, restrictions on funds’ redemption duration could be explored with the aim of aligning investors’ liquidity with the funds’ asset liquidity.[19] The redemption duration is a measure of the time an investor has to wait to withdraw its investment in the fund, which is a combination of a fund’s notice period, the redemption frequency and the lock-up period. Such an instrument could be differentiated based on the fund type, or a limited number of fund “profiles” that represent a combination of key fund characteristics, including the asset and liability side of the fund. By way of example, real estate funds could be required to have a longer redemption duration than equity funds investing in liquid securities. Or, a minimum redemption duration could be considered for funds which are highly leveraged and at the same time invest heavily in illiquid assets. Restrictions on redemption duration may be more effective, more proportional and easier to implement than a liquidity buffer if it is possible to clearly identify the target fund group based on the type or profile.

Price-based measures such as redemption fees or swing pricing are more complex and may only be partially effective in limiting runs. The purpose of redemption fees or swing pricing[20] is to charge redeeming investors the costs associated with their withdrawal from the fund. Absent such price measures, the costs of liquidating assets to satisfy redemptions will only be borne by those investors that stay invested in the fund – creating a first-mover advantage that could trigger a run. Macroprudential authorities could consider providing direction on the use of price-based measures, for instance by providing principles that guide the calibration of fees and swing prices by fund managers, or by setting minimum fee and swing price requirements. This would be complex, since authorities would need to be able to calibrate the “right” fee or swing price for a large universe of asset classes and markets under normal and stressed conditions, and to take into account investors’ behaviour. Moreover, price-based measures may not even be effective in mitigating systemic risk.[21] When investors expect large losses on a fund’s assets, they would be willing to pay a higher price for exiting the fund and the first-mover dynamics would persist.

The power to suspend redemptions provides authorities with a possibly more effective crisis management instrument to halt runs in exceptional circumstances. By requiring fund managers to suspend redemptions in exceptional market conditions, authorities would be able to effectively halt investor runs that contribute to financial stability risk. While fund managers themselves would be able to suspend redemptions, they are mandated to act in the interest of investors, which may not be fully aligned with the public interest of financial stability and may be subject to an inaction bias. Moreover, because of incomplete information and coordination problems, fund managers do not have a view of the financial stability implications of selling assets or applying liquidity management tools. It would be relatively simple for macroprudential authorities to implement the suspension of redemptions in a targeted way during a crisis scenario. The costs to investors, i.e. the loss of access to liquidity for a limited period, would need to be proportional to the financial stability gains, which would most likely also benefit the investors themselves. An additional advantage would be that all investors are treated equally, and that gaming and arbitrage of the measure is less likely. Alternative measures that are available to fund managers as crisis management tools, such as redemption in kind, may be less suitable as a macroprudential instrument. Redemption in kind may effectively mitigate the risk of fire sales and further market disruptions, but may not be efficient in certain cases.[22] Funds’ assets are usually not perfectly divisible and it may therefore be difficult to distribute the assets among the funds’ investors.

Table 1

Assessment of potentially useful macroprudential liquidity instruments for investment funds

Source: Author’s presentation.

Notes: The table provides a preliminary conceptual assessment of the relative effectiveness and efficiency of various possible macroprudential liquidity instruments. The examples in the table do not represent an exhaustive set of conceivable instruments, and the assessment should be viewed as an example of how the framework for evaluating different instruments could be used. The effectiveness of a certain liquidity instrument is determined by its ability to address the risk of fire sales, spillovers to financial institutions, or disruptions in credit intermediation. A liquidity instrument is deemed efficient if the impact of the measure is proportional to the financial stability risks, if the measure is robust to gaming, and if the measure is easy to understand and implement. It is also important to note that the framework does not take into account the joint ‘performance’ of instruments but focuses on effectiveness and efficiency of individual funds. Moreover the diversity of business models of different funds and corresponding risks may require a differentiated approach when restricting liquidity mismatch. This aspect is recognised in the article but not specifically addressed.

4 Conclusion

The FSB and ESRB have expressed concerns about liquidity risks in investment funds and have called for an exploration of the role of macroprudential authorities in addressing these vulnerabilities. The net assets of European funds grew from €6.1 trillion in 2008 to €14.1 trillion in 2016. At the same time, funds increased their risk-taking by investing in less liquid assets and offering shorter-term redemptions. Liquidity mismatches in investment funds can contribute to systemic risk through transmission channels such as fire sales, direct spillovers to other financial institutions and disruptions in credit intermediation. While fund managers generally have liquidity management tools at their disposal to mitigate risks under many foreseeable scenarios, these may not be sufficient to address macroprudential vulnerabilities. The FSB has therefore recommended that authorities consider providing direction on the use of liquidity management tools by fund managers in exceptional circumstances. The ESRB[23] identified the development of macroprudential instruments that address liquidity mismatches at investment funds as a key priority, and has recently called for further guidance on the power of authorities to suspend redemptions[24] – the only liquidity instrument that is currently available to authorities in Europe.

To facilitate further policy discussions in this area, this article provides a conceptual and preliminary assessment of the effectiveness and efficiency of various potential macroprudential liquidity tools for investment funds. The assessment is based on existing ESRB guidance on designing macroprudential instruments. It is meant to inspire further research and policy analysis, and as an encouragement for authorities to further the understanding of macroprudential instruments for the investment fund sector.

The assessment suggests that the suspension of redemptions constitutes a valuable crisis management instrument for authorities, and that structural requirements such as redemption duration restrictions could be explored further with the aim of improving the resilience of funds. By requiring fund managers to suspend redemptions under exceptional circumstances, authorities would be able to effectively halt investor runs that contribute to financial instability. In such crisis scenarios, the benefits to the financial system would seem to outweigh the costs in terms of investors’ temporary loss of access to liquidity. This finding underpins the importance of the ESRB’s recommendation to the European Commission to operationalise the use of suspension of redemptions by national competent authorities as well as of ESMA’s coordinating role[25]. In addition to having a crisis management instrument, it may be worthwhile further exploring structural requirements that aim to improve the resilience of the investment fund sector. The assessment in this article points to the idea of a ‘redemption duration measure’ as a possible useful instrument to align funds’ redemption policies with their liquidity and leverage risks from a macroprudential perspective.

References

Chen, Q., Goldstein, I. and Jiang, W. (2010), “Payoff complementarities and financial fragility: Evidence from mutual fund outflows”, Journal of Financial Economics, Vol. 97, No 2, pp. 239-262.

Doyle, N., Hermans, L., Molitor, P. and Weistroffer, C. (2016), “Shadow banking in the euro area: risks and vulnerabilities in the investment fund sector”, Occasional Paper Series, No 174, European Central Bank, June.

European Central Bank (2017), Financial Stability Review, November.

European Systemic Risk Board (2018), Recommendation on liquidity and leverage risks in investment funds, ESRB/2017/6, 14 February.

European Systemic Risk Board (2017), “The macroprudential use of margins and haircuts”, February.

European Systemic Risk Board (2016), “Macroprudential policy beyond banking: an ESRB strategy paper”, July.

European Systemic Risk Board (2013), Recommendation on intermediate objectives and instruments for macroprudential policy, 4 April.

Financial Stability Board (2017), “Policy Recommendations to Address Structural Vulnerabilities from Asset Management Activities”, 12 January.

Goldstein, I., Jiang, H. and Ng, D. T. (2017), “Investor flows and fragility in corporate bond funds”, Journal of Financial Economics, 126(3), 592-613.

International Monetary Fund (2015), Global Financial Stability Report, April, Chapter 3.

International Organization of Securities Commissions (2015), “Liquidity Management Tools in Collective Investment Schemes: Results from an IOSCO Committee 5 survey to members”, December.

Lewrick, U. and Schanz, J. (2017), “Is the price right? Swing pricing and investor redemptions”, BIS Working Paper No 664, October.

Molestina, L., Wedow, M. and Weistroffer, C. (2017), “Procyclicality, fragility and leverage in bond funds? The impact of leverage on the flow-performance nexus”, unpublished working paper.

Novick, B., Cound, J., Rosenblum, A. and Barry, R. (2017), “Macroprudential Policies and Asset Management”, BlackRock Viewpoint.

Schaub, N. and Schmid, M. (2013), “Hedge fund liquidity and performance: Evidence from the financial crisis”, Journal of Banking & Finance, Vol. 37(3), pp. 671-692.

Stein, J.C. (2005), “Why are most funds open-end? Competition and the limits of arbitrage”, Quarterly Journal of Economics, Vol. 120, No 1, pp. 247-272.

van der Veer, K., Levels, A., Lambert, C., Molestina Vivar, L., Weistroffer, C., Chaudron, R. and de Sousa van Stralen, R. (2017), “Developing macroprudential policy for alternative investment funds: Towards a framework for macroprudential leverage limits in Europe: an application for the Netherlands”, Occasional Paper Series, No 202, European Central Bank, November.

European Central Bank (2017), Financial Stability Review, November, and van der Veer, K., Levels, A., Lambert, C., Molestina Vivar, L., Weistroffer, C., Chaudron, R., and de Sousa van Stralen, R. (2017), “Developing macroprudential policy for alternative investment funds: Towards a framework for macroprudential leverage limits in Europe: an application for the Netherlands”, Occasional Paper Series, No. 202, Euorpean Central Bank, November.

Financial Stability Board (2017), Policy Recommendations to Address Structural Vulnerabilities from Asset Management Activities, 12 January, and European Systemic Risk Board (2016), Macroprudential policy beyond banking: an ESRB strategy paper, July.

Financial Stability Board (2017). Similarly to the FSB, in 2018 the ESRB issued a recommendation to address systemic risks related to liquidity mismatches and the use of leverage by investment funds. One important aspect of the ESRB recommendation relates to authorities’ role should fund redemptions need to be suspended. The ESRB finds it important that the role of national competent authorities (NCAs) should be clarified. More specifically, the European Commission has been asked to propose amendments to the legislation which specify NCAs’ role should they need to exercise their power to suspend redemptions in exceptional circumstances and when there is evidence of cross-border financial stability risks. To this end, the Commission has been asked to clarify the role of the European Securities and Markets Authority (ESMA) in the event of cross-border financial stability implications.

European Systemic Risk Board (2016).

European Systemic Risk Board (2016).

European Systemic Risk Board (2013, 2016, 2017).

See, for example, Stein, J.C. (2005), Doyle, N., Hermans, L., Molitor, P. and Weistroffer, C. (2016) or van der Veer, K., Levels, A., Lambert, C., Molestina Vivar, L., Weistroffer, C., Chaudron, R. and de Sousa van Stralen, R. (2017), specifically Section 2.2. and Box 3.

See, for example, Goldstein, I., Jiang, H. and Ng, D. (2017) and Chen, Q., Goldstein, I. and Jiang, W. (2010).

See, for example, Molestina, L., Wedow, M. and Weistroffer, C. (2017), van der Veer, K., Levels, A., Lambert, C., Molestina Vivar, L., Weistroffer, C., Chaudron, R. and de Sousa van Stralen, R. (2017) and Chen, Q., Goldstein, I. and Jiang, W. (2010).

It should be noted that margin call-related liquidity risk can also occur in closed-ended funds.

European Systemic Risk Board (2016).

Recommendation of the European Systemic Risk Board of 7 December 2017 on liquidity and leverage risks in investment funds (ESRB/2017/6).

Article 46 of the Alternative Investment Fund Managers Directive and Article 98(2)(j) of the UCITS Directive allow authorities to suspend redemptions if this is “in the interest of the shareholder or in the interest of the public”.

Recommendation of the Euorpean Systemic Risk Board of 4 April 2013 on intermediate objectives and instruments for macroprudential policy (ESRB/2013/1).

Van der Veer, K., Levels, A., Lambert, C., Molestina Vivar, L., Weistroffer, C., Chaudron, R. and de Sousa van Stralen, R. (2017).

It is important to note that clear guidance on the use of crisis management tools is needed in order to mitigate potential macroprudential trade-offs and potential coordination problems. While the suspension of redemptions, for example, halt runs, it may also send a negative signal to investors and markets. More specifically, redemption suspensions may have a direct adverse impact on the confidence of investors in the fund and/or the reputation of the fund. At the same time, they may also have an impact on funds with similar profiles or of a similar type even if they have not suspended redemptions, which could face withdrawals as a consequence.

Novick, B., Cound, J., Rosenblum, A. and Barry, R. (2017) state that liquidity buffers “would lead to procyclical outcomes”, as fund managers would be encouraged “to sell less liquid assets in order to maintain their mandatory liquidity buffers”. Moreover, the authors state that “investors (…) [may be incentivised to] retreat when their participation might otherwise be stabilizing”. To prevent such behaviour and to be clear about the concept of liquidity buffers considered in this article, it should be noted that the idea is that buffers are allowed to be used to meet liquidity demands under certain conditions. In exceptional circumstances, fund managers would be able to deplete buffers, which implies that funds would not need to meet requirements. As a consequence, fund managers would not need to only sell the least liquid assets. Moreover, to manage investor expectations and to mitigate potential additional run risk, investors would need to be provided with additional information and guidance. In practical terms, clear information and guidance should also be provided to the industry stating when/under what circumstances a fund would be allowed to deplete liquidity buffers and until when/under what circumstances funds would be required to stock them up.

It is acknowledged that further work on liquid assets would be warranted to provide a more nuanced assessment of the suitability of liquidity buffers for macroprudential purposes. In this regard, it should be noted that the ESRB has recommended that ESMA develop a list of illiquid assets (see footnote 12). Further work should provide a more differentiated analysis of how liquidity buffers function from an individual fund perspective versus a systemic perspective, taking into account how the liquidity of assets may differ between normal times and stressed circumstances. Moreover, linkages to other financial sector participants should be considered.

Rules for aligning funds’ investment strategies with redemption profiles already exist today, e.g. in the United States in the form of SEC Rule 22e-4. However, such rules may also be complex as asset risk assessments may be dependent on market conditions.

Swing pricing is mechanism by which long-term shareholders are protected against the dilution impact of securities trading that relates to investors entering or exiting the fund. More specifically, swing pricing occurs when a fund provider adjusts the net asset value (NAV) of a fund in order to pass on the costs of trading to those investors that are buying and selling within their accounts. In practice, swing pricing increases the price of a fund share above its NAV when the fund is experiencing exceptional inflows, and decreases it when the fund is experiencing exceptional outflows. In this way, the negative externality caused by trading investors that affects remaining investors is internalised, and the first–mover advantage is reduced or removed. There are two types of swing pricing: “full” and “partial”. With full swing pricing, the price will move regardless of the size of the net flows, whereas with partial swing pricing the price is adjusted only if the net capital flows exceed a predetermined threshold, which is aligned with the time of dilution.

Lewrick, U. and Schanz, J. (2017) find that swing pricing has limited effects during stress episodes. More specifically, comparing Luxembourg and US funds, the authors find that current swing pricing rules based on applying a constant swing factor when outflows exceed a certain threshold are unlikely to counteract first-mover behaviour in stressed market conditions. It is important to note that the empirical analysis uses the fact that swing pricing is available to Luxembourg funds and not to US funds.

It should be noted that redemption in kind can prove effective and efficient for exchange-traded funds (ETFs). The reason is that authorised participants (APs) have exclusive access to the ETF primary market. This implies that in contrast to mutual funds, APs can only redeem ETF shares. Investors transact ETF shares with each other in secondary markets.

European Systemic Risk Board (2016).

Recommendation of the European Systemic Risk Board of 7 December 2017 on liquidity and leverage risks in investment funds (ESRB/2017/6).

See Recommendation of the European Systemic Risk Board of 7 December 2017 on liquidity and leverage risks in investment funds (ESRB/2017/6). When it comes to the suspension of redemptions, the ESRB considers it important that the role of NCAs should be clarified. The European Commission has been asked to propose amendments to the legislation which specify NCAs’ role should they need to exercise their power to suspend redemptions in exceptional circumstances and when there is evidence of cross-border financial stability risks. In this regard, the Commision has been asked to clarify ESMA’s role in the event of cross-border financial stability implications.