Buffer use and lending impact

This article explores the role of capital buffers in containing the reduction of lending to the real economy during the COVID-19 crisis. The assessment compares the results when banks are willing to use the buffers with the outcomes when they refrain from using the buffers by using the macro-micro model BEAST. Our results show that banks’ use of capital buffers leads to better economic outcomes, without a negative impact on their resilience. Banks’ willingness to use capital buffers is reflected in higher lending, with positive effects on GDP and lower credit losses, while the resilience of the banking system is not compromised.

1 Introduction

The outbreak of the coronavirus (COVID-19) pandemic and the subsequent enforcement of containment measures have been a severe shock to European economies. As past experience shows, adverse exogenous shocks which trigger simultaneous capital losses and liquidity strains in multiple financial institutions can prompt lending contractions. By shrinking their balance sheets financial institutions can generate externalities in the form of adverse macro-financial feedback loops, further aggravating adverse macroeconomic outcomes.

The revised Basel framework, known as Basel III, introduced a new instrument aimed at addressing the risks of adverse macro-financial feedback loops, namely capital buffers. These include countercyclical capital buffers, which are designed to be released at times of economic adversity, just as a number of countries have done in response to COVID-19 developments. However, a much larger set of structural and conservation buffers can be drawn down to absorb losses or to maintain lending under adverse conditions. Banks dipping into their capital buffers become subject to profit distribution restrictions rather than insolvency procedures, as would be the case with hard capital requirements. In a recessionary environment, capital buffers are an additional layer of usable capital to support lending and cover losses, thereby smoothing the downturn of business or credit cycles.

This paper looks at the role of capital buffers in containing the reduction of lending to the real economy during the COVID-19 crisis. The assessment is performed using the banking euro area stress test model (BEAST) in a counterfactual manner, namely by comparing the results when the buffer is used with the outcomes in its absence. The assessment is performed using two alternative scenarios from the vulnerability assessment exercise,[1] assuming a central and a severe future economic path, respectively. Both scenarios assume a contraction in GDP in 2020 owing to lockdown measures and differ in the intensity and length of the recession. The assessment addresses the following questions. First, do greater supervisory flexibility and the use of released capital reserves adversely affect the soundness of banks measured in terms of credit losses, profitability and solvency rates? Second, how do the mitigating actions regarding buffer use contain the amplification effects stemming from the banking sector-real economy feedback loop?

The macro-micro model BEAST (Budnik et al., 2020) incorporates detailed, up-to-date information about existing bank-level capital requirements and balance sheets of 91 significant institutions. The model also allows banks to flexibly adjust their balance sheets to economic conditions and changing risks. This involves adjustments to profit distributions, lending volumes and pricing of loans, and changes in liability structures. These behavioural responses are based on empirical estimated equations employing bank-level data. Bank reaction introduces two amplification mechanisms: the feedback loop between bank solvency and funding costs, and the feedback loop between the real economy and the banking sector. The model controls for the key transmission channels through which buffer use is expected to operate.

Our results show that banks’ use of capital buffers leads to better economic outcomes, without much negative impact on their resilience. Banks’ willingness to use capital buffers is reflected in higher lending, with positive effects on GDP and lower credit losses, while the resilience of the banking system is not compromised. Estimates show that, in stressed scenarios, a broad-based use of capital buffers could increase lending to the real economy by more than 3%, and GDP by over 0.5%. The resulting positive impact on economic activity reduces credit losses and sustains banks’ profitability, while Common Equity Tier 1 (CET1) ratios remain essentially unaffected. Overall, our results argue in favour of countercyclical regulation that encourages banks to retain earnings and build up capital buffers in good times and relaxes constraints in downturns.

Our findings complement empirical and simulation-based studies that argue in favour of countercyclical capital buffers. Most of the available research shows that an increase in the countercyclical capital buffer (CCyB) reduces excessive lending (Drehmann and Gambacorta, 2012; Aikman et al., 2015; Rubio and Carrasco-Gallego, 2016), mitigates credit imbalances (Brzoza-Brzezina et al., 2015), curbs credit cycles (Tayler and Zilberman, 2016; Gersbach and Rochet, 2017; Kanngiesser et al., 2019) and limits system-wide losses (Bui et al., 2017). A common feature of the above research is that the focus is on the build-up phase of financial vulnerabilities, whereas we analyse how the buffer release cushions the crisis.

The remainder of this article is organised as follows. Section 2 describes policy measures in response to the COVID-19 pandemic and discusses implications and existing evidence on the use of buffers. Section 3 briefly describes the model. In Section 4 we present our main findings. Section 5 concludes and discusses policy implications.

2 COVID-19 developments and capital buffers

The COVID-19 pandemic is a rare type of shock to the world economy. Unlike the great recession of 2008 and the European debt crisis of 2011-12, the shock originated not from the financial system, or even the economic system, but from the biosphere. Nevertheless, the spread of the coronavirus and the significant efforts to contain its spread have created disruptions in many world economies and turbulence in financial markets. The economic policy response to the crisis has been unprecedented. All countries affected have immediately undertaken initiatives comprising a combination of extensive government fiscal stimulus packages, central bank liquidity and monetary policy measures, and actions relating to the application of micro- and macroprudential regulations.

Procyclical behaviour of the financial system, and especially of banks, implies that financial intermediaries amplify swings in economic activity. The strength with which the amplification mechanism operates depends on, among other things, financial imbalances accumulated in the pre-crisis period (e.g. credit growth, leverage and maturity mismatches) (Constâncio et al., 2019). For example, weakly capitalised banks, when under intense stress from a solvency or liquidity perspective, are more likely to deleverage or sell assets in fire sales, thereby potentially creating further problems in other areas of the interconnected financial system. Such procyclical behaviour among financial intermediaries could significantly amplify the downturn, particularly if financial intermediaries become capital-constrained or risk-averse (Darracq-Pariès et al., 2019).

The reaction of banks to adverse shocks depends not only on their initial but also on their target levels of capitalisation, with the latter being closely related to the regulatory setup. The extent to which banks decide to curb credit to the economy after an initial shock materialises is therefore contingent on the supervisory stance. Even viable banks that comply with minimum capital requirements and have not used up their capital buffers may decide to cut back loans to shore up their capital positions and satisfy supervisory expectations. The direct gain from strengthening their capital position would be small, however, and the costs to the wider economy – and hence the banking system – much larger. A countercyclical capital framework should therefore allow policy responses to be calibrated in a way that enables banks to provide financing to the real economy without compromising their resilience.

An important element of the new Basel III regulatory framework is capital buffers, which are designed to increase banks’ resilience to macro-financial shocks and reduce procyclicality and excessive amplification of the financial cycle.[2] The various buffers included in the framework differ in the degree to which they lean towards one or other of these two objectives. For example, the capital conservation buffer (CCoB) leans towards the first objective, whereas the CCyB also tackles the second objective, as it can be set to zero when stress materialises. Buffers for global and other systemically important institutions (G-SIIs and O-SIIs) and the systemic risk buffer (SyRB) are meant to provide additional loss-absorbing capacity for a specific set of institutions.

Capital buffers were not designed for proactive management of the macroeconomy. However, they can support bank lending in times of stress. Once initial losses have been absorbed, banks can use what remains in their buffers to extend their balance sheets in order to support credit expansion. The release of regulatory buffers thus gives banks more flexibility to adjust their balance sheets, alleviating economic tensions during the crisis and recovery period, and can counter the procyclical behaviour of banks. Moreover, early recognition of losses is desirable as it makes crisis episodes shorter and less intense (Beatty and Liao, 2011; Homar and van Wijnbergen, 2015).

There is little evidence on the effects of the release of capital buffers. This reflects the relatively short period that these policy instruments have been available. The literature on the effects of capital releases either focuses on past episodes of released capital or studies the impact in aggregate simulation-based models. The latter group of studies often apply to a wider geographical area, but can only approximate a capital release through changes in bank capital ratios (see, for example, Gross et al., 2016; and Noss and Toffano, 2016). Jimenez et al. (2017) and Sivec et al. (2019) study the impact of bank capital release at the beginning of the global financial crisis. Jiménez et al. (2017) study the effects of dynamic provisioning on the supply of credit to firms in good times and bad. Sivec et al. (2019) provide empirical evidence on the effectiveness of capital buffer release based on the policy experiment in Slovenia where the central bank unexpectedly released capital buffers at the start of the financial crisis. Using detailed credit register data in a difference-in-differences setup (Khwaja and Mian, 2008), both papers find a positive effect of released capital on loan supply. Jiménez et al. (2017) show that dynamic provisioning smooths credit supply cycles and, in bad times, supports firm performance. Sivec et al. (2019) show that by releasing capital buffers, increased lending to the economy was mainly directed towards healthy firms, which is a desirable outcome for policymakers and banking regulators.

Even though studies show the benefits of released capital, banks might not always be willing to use it [see article 1 for reference]. Lowering capital ratios by exhausting all buffers could expose banks to significant risks, especially in combination with high uncertainty about the future economic path (Lewrick et al., 2020). In addition, there might be expectations among markets, investors and counterparties, or peer pressure to preserve a certain level of capitalisation and not to let it drop to the regulatory minimum. As discussed by Drehmann et al. (2020), approaching the regulatory minimum is usually avoided, as it is associated with the point of non-viability. Furthermore, low capitalisation can affect banks’ profitability through lower credit ratings and higher funding costs (Gambacorta and Shin, 2018).

Although supervisors and regulators have limited ability to influence banks to behave countercyclically and draw down buffers to extend credit to the economy, they can eliminate barriers and impediments that disincentivise banks from doing so. One form of action is to prompt banks to expand lending by communicating the advantages of coordinated action. In its communication of 12 March, the ECB indicated that banks were expected to use the capital release package to support the economy.[3] On 22 March, the ECB introduced further supervisory flexibility measures to ensure that “banks can continue to fulfil their role to fund households and corporations”.[4] The use of buffers to support the economy is also strongly supported by the Bank of England, which showed that the economic shock would need to be twice as big as in the current central projection to incur losses in excess of the amount of capital buffers.[5]

Authorities can separate the use of any buffers from dividend pay-outs by imposing restrictions on the latter. In fact, most of the supervisory authorities in Europe have already extended recommendations on banks’ dividend policy and clarified a timeline to restore buffers.[6] The ECB extended its recommendation to banks on dividend distributions and share buy-backs until 1 January 2021 and asked banks to be extremely moderate with regard to variable remuneration. This action was taken “to boost banks’ capacity to absorb losses and support lending to households, small businesses and corporates during the coronavirus (COVID-19) pandemic”.[7]

More directly, authorities can encourage the use of buffers by temporarily exempting banks from replenishing drawn-down resources, which may be costly for banks if requested too abruptly. For example, the ECB made it clear that it will give banks enough time to replenish their capital and liquidity buffers in order not to act procyclically.[8] The ECB has committed itself to allowing banks to operate below the P2G and the combined buffer requirement until at least the end of 2022, and below the liquidity coverage ratio until at least the end of 2021.

Finally, and in line with the emphasis on the role of lending, authorities can communicate the advantages of using buffers. On 28 July the ECB published results of a simulation-based analysis showing clear benefits of buffer use, which leads to higher lending and higher economic activity. In turn, banks’ profitability would be positively affected, mainly via lower credit losses.[9] Similarly, the Bank of England showed through stress test analysis that the UK economy and banking system would be weakened if banks started defending their own financial position.[10] It is therefore in the interest of banks and the economy as a whole that banks use the buffers as much as possible and continue supporting businesses and households.

3 Model

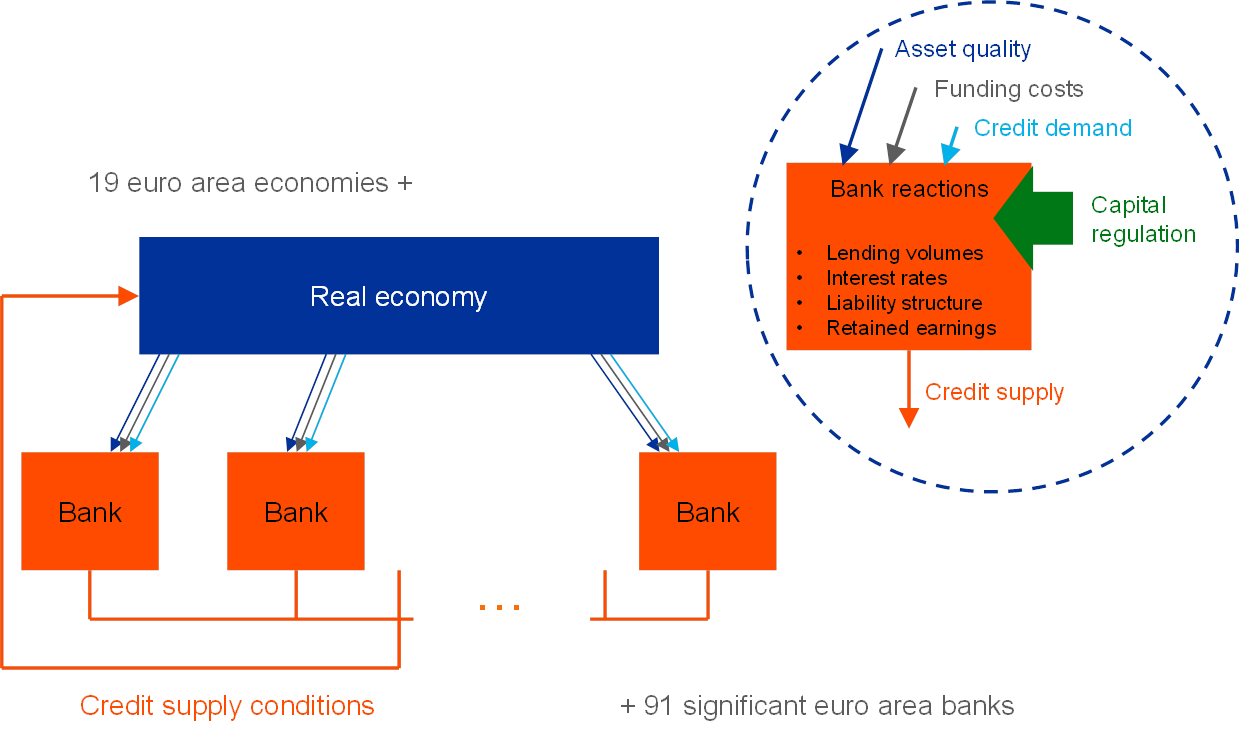

The exercise is conducted using the macro-micro model BEAST, which is a large-scale, semi-structural model linking macro and bank-level data. The model captures the heterogeneous behaviour of individual banks and includes interactions between the financial sector and the real economy.[11] It covers 91 of the largest euro area banks with their individual balance sheets and profit and loss accounts in 19 euro area economies. The sample of banks covers broadly 70% of the euro area banking sector in terms of total assets, allowing a detailed analysis of the impact of policy actions regarding the use of buffers on banks across euro area economies.

The model looks at dynamic adjustments of banks and economies. The approach focuses on modelling banks’ adjustments of loan and other asset volumes and behavioural responses on their liability structure (see Figure 1). It also projects the evolution of loan pricing, funding costs and profit distribution policies in line with empirical bank-level evidence. Finally, the model aggregates the impact of these individual bank responses on the credit supply and lending rates to the real economy, thereby capturing dynamic interdependencies of aggregate real and financial variables. Thus, in the model, a stress simulation solves simultaneously for macroeconomic and bank-specific outcomes, ensuring micro-to-macro consistency. There is no sequential separation between the scenario design and banks’ financial developments as is otherwise common in standard stress testing exercises.

Figure 1

Schematic illustration of the BEAST model

Sources: The chart is taken from Budnik et al. (2019).

The model captures amplification effects through banks’ adjustments in the presence of solvency constraints. More specifically, in an adverse scenario, banks experience losses and a deterioration of their balance sheets. After the realisation of losses and credit risk parameter adjustments, banks rebalance their portfolios to mitigate capital shortfalls and to restore their solvency levels. The capital shortfall of a given bank is defined as the (negative) difference between its actual CET1 capital ratio and its target CET1 ratio calculated as the sum of minimum capital requirements, P2R, capital buffers and P2G. The feedback loop from the banking system to the real sector relates to a credit supply shock in the form of a non-linear credit supply reaction to banks’ capital shortfalls.

The buffer use exercise is performed with a counterfactual exercise which compares the results before and after a hypothetical policy change. The key adjustments in the model that affect banks and the real sector relate to banks’ capital targets and distribution of dividends. First, the policy actions aimed at releasing the buffers result in a reduction in banks’ capital targets, which are closely linked to regulatory thresholds. Second, the regulatory pay-out restrictions in the euro area constrain banks from paying out any dividends in 2020.[12] Because bank lending responds endogenously to changing capitalisation relative to capital targets, the higher level of available capital (that is not distributed to shareholders) is expected to lead to higher lending when compared to the outcome without it. In addition, the positive impact of the release of buffers should be boosted through second-round effects. An improved macroeconomic outlook would further strengthen lending and have a positive effect on credit losses, average risk weights and the share of non-performing loans (NPLs).

4 Findings

The European banking sector has built up a significant amount of capital buffers since the global financial crisis of 2007-09 (see Chart 1). This means that the sector entered the COVID-19 pandemic crisis more resilient, which allows it to absorb rather than amplify the macroeconomic shock. Banks currently operate with a buffer equal to 3.5% of risk-weighted assets (RWA), while 2% was already released on 12 March when the ECB allowed banks to operate below the level of capital defined by P2G. This shows that banks can use the additional buffers to further support lending in the turbulent economic conditions caused by lockdown measures related to the outbreak of COVID-19.

Chart 1

Releasable capital as a percentage of RWA

Sources: authors’ calculations based on ECB data.

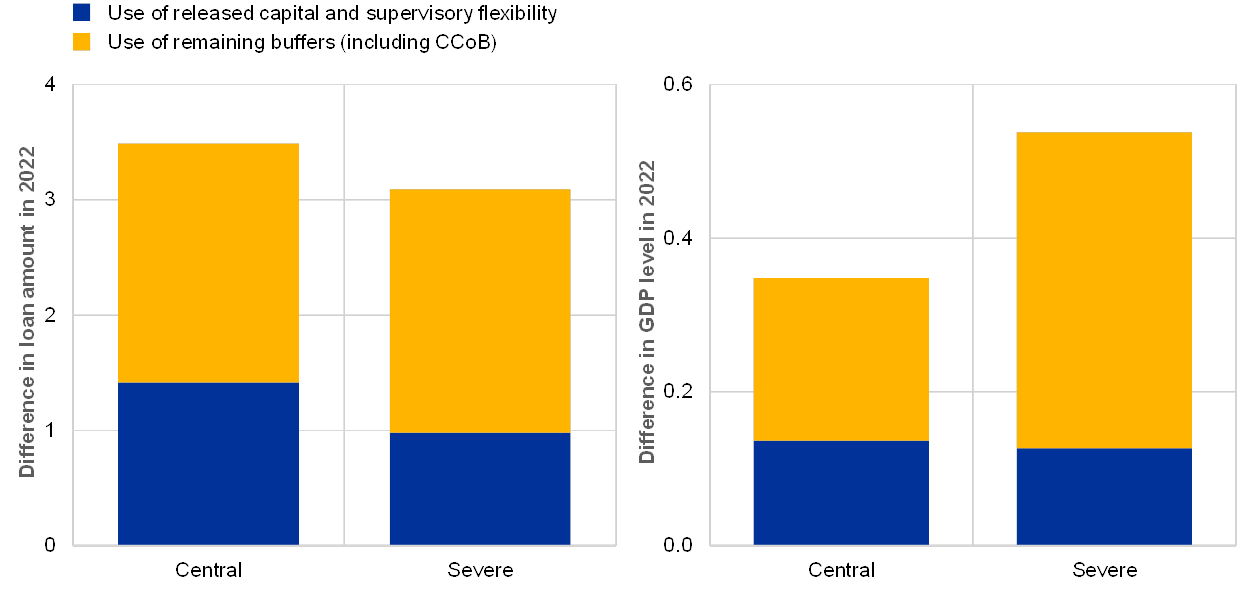

Using the available buffers is expected to increase lending to the non-financial private sector by more than 3% in both scenarios when compared to a situation in which the buffers are not used.[13] The impact is stronger in the less severe (central) scenario, as in this case the demand for loans is stronger and can take greater advantage of the increased loan supply stemming from the use of the buffers. Looking across sectors, the released capital is of most benefit to non-financial corporations (NFCs), for which lending increases by 7.8% in the central scenario and by 5.3% in the severe scenario. This reflects higher sensitivity of NFC lending to released capital, which at the same time also increases the effectiveness of the guaranty policies. The increase in lending supports economic activity, resulting in 0.3 to 0.5% higher GDP in 2022 when banks use the available buffers (see Chart 2).

Chart 2

Buffer use in support of lending and economic activity

(left panel: impact on lending; right panel: impact on GDP, percentage points)

Sources: authors’ calculations based on ECB data.

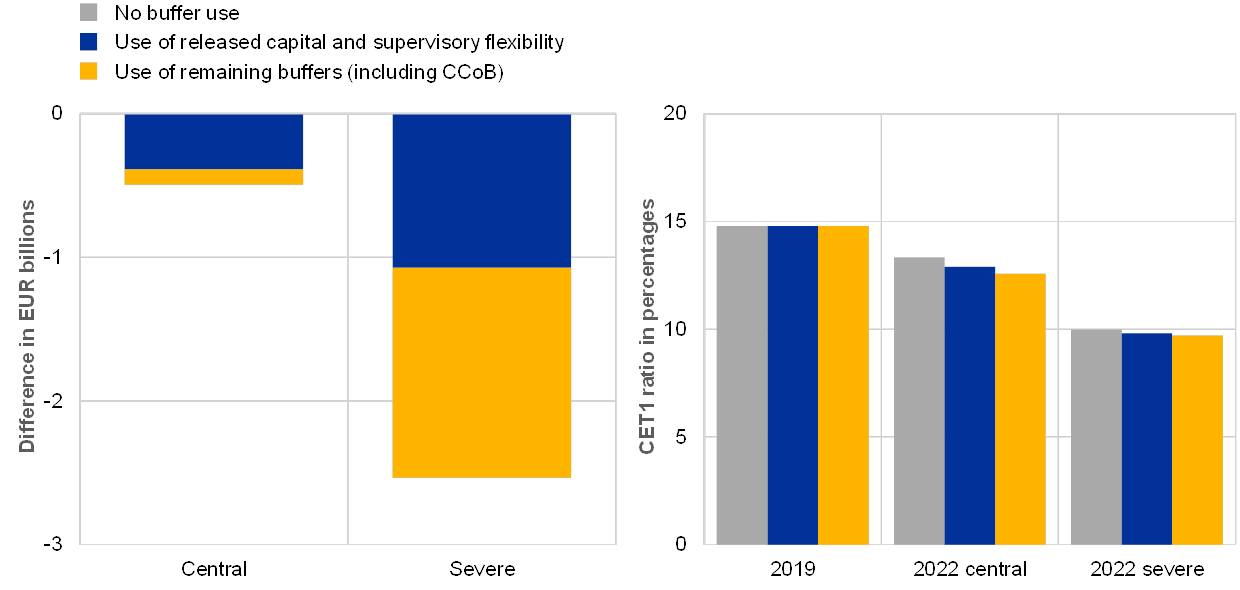

Buffer use has positive second-round effects. Because the use of buffers improves the future economic outlook, it has positive effects on bank vulnerability and profitability. When banks use their buffers, they are expected to experience lower transitions to default, resulting in a 0.2 percentage point lower NPL ratio in 2022. In turn, and also taking into account positive effects on loss given default, credit losses are expected to be lower (see Chart 3). This is especially pronounced in the severe scenario, where credit losses are €2.5 billion lower. Similarly, net interest income also increases most in the severe scenario, by €4 billion, contributing to a positive overall effect of capital release on bank profitability.

Chart 3

Lower credit losses and same solvency

(left panel: impact on credit losses; right panel: impact on CET1 ratio, percentage points)

Sources: authors’ calculations based on ECB data.

The CET1 ratio is only marginally affected when banks use their buffers. In the central and severe scenarios, the CET1 ratio is projected to decrease from about 15% in 2019 to 13% and 10%, respectively, when banks preserve the buffer (see Chart 3). Even though the released buffer significantly lowers capital requirements, the CET1 ratio is only around 0.7 percentage points lower when the buffer is used. The decrease in the CET1 ratio is higher for banks with a larger release of capital requirements, and this association is stronger in the central scenario.

5 Conclusions

This article assesses the impact of buffer use on lending, real economic activity and bank resilience. The results of our simulation provide additional evidence that drawing on buffers in a downturn can be of benefit for the economy and for banks themselves. The use of capital buffers supports lending and prevents further deterioration in economic activity. The resulting lower incidence of credit defaults translates into a relative increase in banks’ profitability and their capacity to rebuild capital buffers. In consequence, what matters most is banks’ intention to use buffers rather than their actual use. However, in order to generate the virtuous economic effects, the willingness to temporarily use capital buffers needs to be as broad as possible.

Capital buffers were designed to mitigate negative second-round effects of the crisis via the banking system. Model simulations referring to two alternative scenarios illustrating the developments after the COVID-19 crisis, and employing the most up-to-date information about banks’ balance sheets, show that banks’ willingness to use buffers can have a material impact on the severity and duration of the recession.

The analysis is conditional on a number of modelling assumptions, but one caveat in particular is worth mentioning. The analysis does not consider the question of why banks might use or refrain from using their capital buffers. While it recognises that the non-use of capital buffers is a form of coordination failure, where individually rational actions lead to inferior results for banks and the real economy, it remains silent about incentives that would make banks more willing to use their capital buffers.

References

Aikman, D., Haldane, A.G. and Nelson, B.D. (2015), “Curbing the credit cycle”, The Economic Journal, Vol. 125(585), pp. 1072‑1109.

Bahaj, S., Bridges, J., Malherbe, F. and O’Neill, C. (2016), “What determines how banks respond to changes in capital requirements?”, Staff Working Paper, No 593, Bank of England.

Beatty, A. and Liao, S. (2011), “Do delays in expected loss recognition affect banks’ willingness to lend?”, Journal of Accounting and Economics, Vol. 52(1), pp. 1‑20.

Brzoza-Brzezina, M., Kolasa, M. and Makarski, K. (2015), “Macroprudential policy and imbalances in the euro area”, Journal of International Money and Finance, Vol. 51, pp. 137‑154.

Budnik, K.B., Balatti Mozzanica, M., Dimitrov, I., Groß, J., Kleemann, M., Reichenbachas, T., Sanna, F., Sarychev, A., Siņenko, N. and Volk M. (2020), “Banking Euro Area Stress Test Model”, Working Paper Series, No 2469, ECB.

Budnik, K.B., Balatti Mozzanica, M., Dimitrov, I., Groß, J., Hansen, I., di Iasio, G., Kleemann, M., Sanna, F., Sarychev, A., Siņenko, N. and Volk, M. (2019), “Macroprudential stress test of the euro area banking system”, Occasional Paper Series, No 226, ECB.

Bui, C., Scheule, H. and Wu, E. (2017), “The value of bank capital buffers in maintaining financial system resilience”, Journal of Financial Stability, Vol. 33, pp. 23‑40.

Constâncio, V., Cabral, I., Detken, C., Fell, J., Henry, J., Hiebert, P., Kapadia, S., Nicoletti Altimari, S, Pires, F. and Salleo, C. (2019), “Macroprudential policy at the ECB: Institutional framework, strategy, analytical tools and policies”, Occasional Paper Series, No 227, ECB.

Darracq-Pariès, M., Fahr, S. and Kok, C. (2019), “Macroprudential space and current policy trade-offs in the euro area”, Financial Stability Review, ECB, May.

Drehmann, M. and Gambacorta, L. (2012), “The effects of countercyclical capital buffers on bank lending”, Applied Economics Letters, Vol. 19(7), pp. 603‑608.

Drehmann, M., Farag, M., Tarashev, N. and Tsatsaronis, K. (2020), “Buffering Covid-19 losses – the role of prudential policy”, BIS Bulletin, No 9, Bank for International Settlements.

Gambacorta, L. and Shin, H.S. (2018), “Why bank capital matters for monetary policy”, Journal of Financial Intermediation, Vol. 35(B), pp. 17‑29.

Gersbach, H. and Rochet, J.-C. (2017), “Capital regulation and credit fluctuations”, Journal of Monetary Economics, Vol. 90, pp. 113‑124.

Gross, M., Kok, C. and Zochowski, S. (2016), “The impact of bank capital on economic activity – Evidence from a Mixed-Cross-Section GVAR model”, Working Paper Series, No 1888, ECB.

Homar, T. and van Wijnbergen, S. (2015), “On Zombie Banks and Recessions after Systemic Banking Crises”, CEPR Discussion Papers, No 10963, Centre for Economic Policy Research.

Jiménez, G., Ongena, S., Peydró, J.L. and Saurina, J. (2017), “Macroprudential Policy, Countercyclical Bank Capital Buffers, and Credit Supply: Evidence from the Spanish Dynamic Provisioning Experiments”, Journal of Political Economy, Vol. 125(6), pp. 2126‑2177.

Kanngiesser, D., Martin, R., Maurin, L. and Moccero, D. (2019), “The macroeconomic impact of shocks to bank capital buffers in the Euro Area”, The B.E. Journal of Macroeconomics, Vol. 20(1).

Khwaja, A.I. and Mian, A. (2008), “Tracing the Impact of Bank Liquidity Shocks: Evidence from an Emerging Market”, American Economic Review, Vol. 98(4), pp. 1413‑1442.

Lewrick, U., Schmieder, C., Sobrun, J. and Takáts, E. (2020), “Releasing bank buffers to cushion the crisis – a quantitative assessment”, BIS Bulletin, No 11, Bank for International Settlements.

Noss, J. and Toffano, P. (2016), “Estimating the impact of changes in aggregate bank capital requirements on lending and growth during an upswing”, Journal of Banking & Finance, Vol. 62, pp. 15‑27.

Rubio, M. and Carrasco-Gallego, J.A. (2016), “Coordinating macroprudential policies within the Euro area: The case of Spain”, Economic Modelling, Vol. 59, pp. 570‑582.

Sivec, V., Volk, M. and Chen, Y. (2019), “Empirical Evidence on the Effectiveness of Capital Buffer Release”, Bank of Slovenia Working Papers, No 5/2019, Banka Slovenije.

Tayler, W.J. and Zilberman, R. (2016), “Macroprudential regulation, credit spreads and the role of monetary policy”, Journal of Financial Stability, Vol. 26, pp. 144‑158.

- See COVID-19 Vulnerability Analysis – Results overview, ECB, 28 July 2020.

- European banking law defines three types of own funds. Common Equity Tier 1 (CET1) capital is the highest quality of own funds and is mainly composed of shares and retained earnings from previous years. Additional Tier 1 (AT1) capital and Tier 2 capital can be equity or liability instruments and are of lower quality. Pillar 2 capital consists of two parts. One is Pillar 2 requirements (P2R), covering risks which are underestimated or not sufficiently covered by Pillar 1. The other is Pillar 2 guidance (P2G), which indicates to banks the adequate level of capital to be maintained in order to have a buffer to withstand stressed situations, in particular as assessed on the basis of the adverse scenario in supervisory stress tests. There are also capital buffers to mitigate specific risks (CCoB, CCyB, SyRB, G-SIIs/O-SIIs). In the event of a bank’s capital falling below the combined buffer requirement (CCoB, CCyB and systemic buffers), banks can make distributions only within the limits of the maximum distributable amount (MDA) as defined by EU law.

- See “ECB Banking Supervision provides temporary capital and operational relief in reaction to coronavirus”, press release, ECB, 12 March 2020.

- See “ECB Banking Supervision provides further flexibility to banks in reaction to coronavirus”, press release, ECB, 20 March 2020.

- See Financial Stability Report, Bank of England, August 2020.

- For example, the Bank of England set out its supervisory expectation that banks should not increase dividends or other distributions, such as bonuses, in response to its policy actions.

- See “ECB asks banks not to pay dividends until at least October 2020”, press release, ECB, 27 March 2020.

- See “ECB extends recommendation not to pay dividends until January 2021 and clarifies timeline to restore buffers”, press release, ECB, 28 July 2020.

- See Enria, A., “The coronavirus crisis and ECB Banking Supervision: taking stock and looking ahead”, The Supervision Blog, ECB, 28 July 2020.

- See Interim Financial Stability Report, Bank of England, May 2020.

- For more detailed description of the model and earlier example of its use, see Budnik et al. (2019) and Budnik et al. (2020).

- After 2020 the resulting dividend pay-outs of banks follow an estimated behavioural rule, taking into account the MDA rule in European banking law.

- The effects presented are decomposed into two sources of buffer usability: “Use of released capital and supervisory flexibility” includes use of P2G, CET1 capital released with the front loading of P2R changes, and released macroprudential buffers. “Use of remaining buffers (incl. CCoB)” concerns the use of all capital above P1R and P2R, with MDA restrictions still binding.